“How puzzling all these changes are! I’m never sure what I’m going to be, from one minute to another.”

Alice from Alice in Wonderland by Lewis Carroll

So far 2025 seems to be a page taken out of Lewis Carroll’s classic Alice in Wonderland. Although we haven’t yet seen the Red Queen or the Mad Hatter the way the year is shaping up, we cannot entirely rule out those possibilities. We have seen a market correction, as defined by a decline in the stock market index from peak to trough of at least 10%, full blown rallies in stock prices that have seen the markets add near 3% to their value in a matter of days, and a constant flow of announcements coming out that drive investor sentiment swinging wildly between despair and euphoria.

Despite the volatility, our approach at Cypress has remained grounded in a steady, long-term view. We continue to focus on diversification and strategic asset allocation to potentially minimize risk while seizing potential opportunities in the market. While the S&P 500 in the first quarter of 2025 ended down 4.59%[1], other segments of the market demonstrated resilience in the face of turbulence and turned positive returns. It is a reminder that while the markets may be unpredictable in the short term, patience and disciplined investment strategies may still yield positive results over time.

As we navigate through these unpredictable times, we want to reassure you that we are closely monitoring the developments in the financial markets, adjusting portfolios where necessary, and continuing to work on your behalf to secure your long-term financial goals. We understand that the market’s emotional rollercoaster can create anxiety, but we are here to help you stay the course, making decisions that aim to align with your objectives, not the day-to-day fluctuations.

Equities

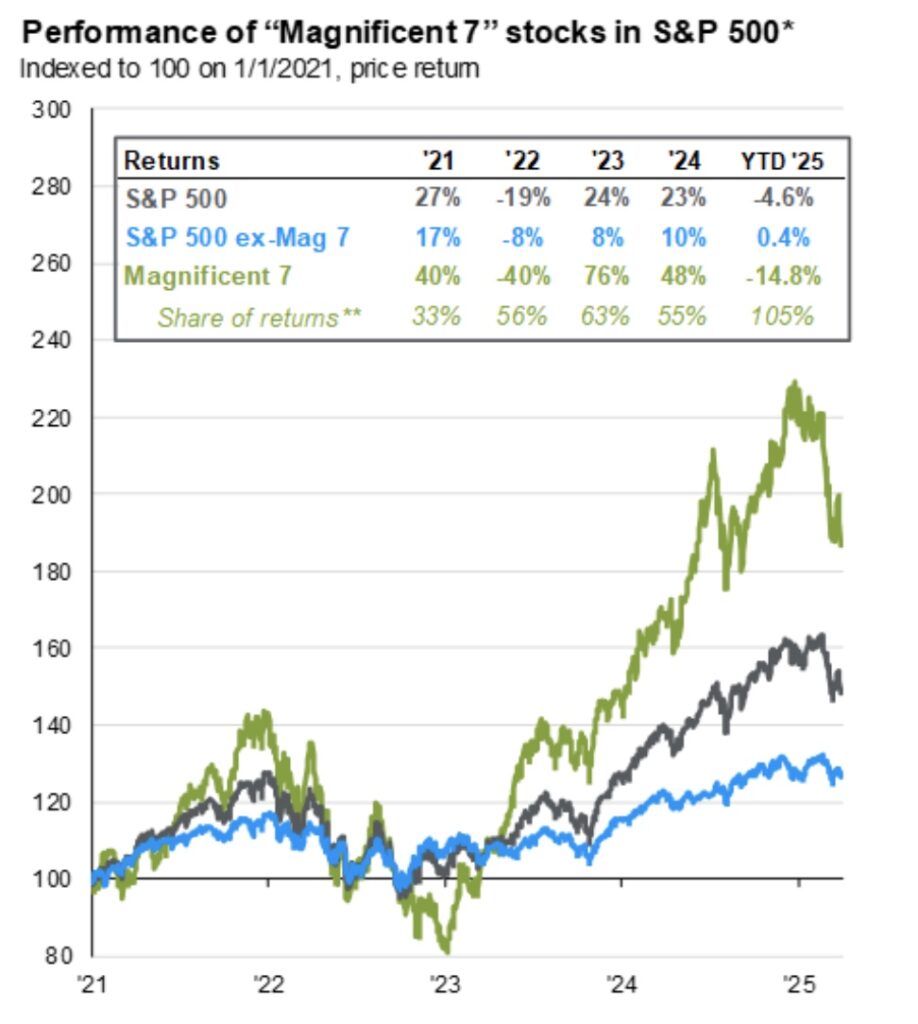

The first quarter of 2025 the S&P 500 Index was down 4.6% following a stellar 2024 that saw the index return over 23%. S&P 500 earnings in the fourth quarter of 2024 grew by 17.1%, with 74% of the companies surprising on the upside and 19% on the downside. Revenue growth for the index was not as strong but still managed to grow 5.1% in the fourth quarter[2]. The Information Technology sector, representing over 30% of the S&P 500, had a drawdown of –11.2%[3] since the beginning of 2025. We have also seen the Magnificent Seven stocks significantly underperforming the other 493 stocks in the S&P 500 in the first quarter, -14.8% vs. 0.4%[4], respectively.

The volatility in this quarter began late January when a Chinese Artificial Intelligence company called “DeepSeek” released its newly developed AI model reporting to have needed a much smaller investment than some of the large U.S hyperscale companies. Adding to the mix is the high valuation that the technology sector had, starting the year with a Price to Earnings ratio of 32.4, and if any news comes out that does not rhyme with perfection it would have and will cause volatility in this sector. On the flip side, the energy sector has enjoyed the best returns since the start of this year, gaining 10%[5], despite the price of oil decreasing in this period. As some of those companies with high valuations face uncertainty, investors are rotating to companies with lower valuations than the S&P 500 such as the ones in the Energy sector, its current price to earnings ratio is 15.7 vs. 20.9[6] of the broader market which would explain the outperformance we have seen thus far in the Energy sector. However, the year is not over yet and there are still many questions and uncertainties the market is waiting on for resolution.

Fixed Income

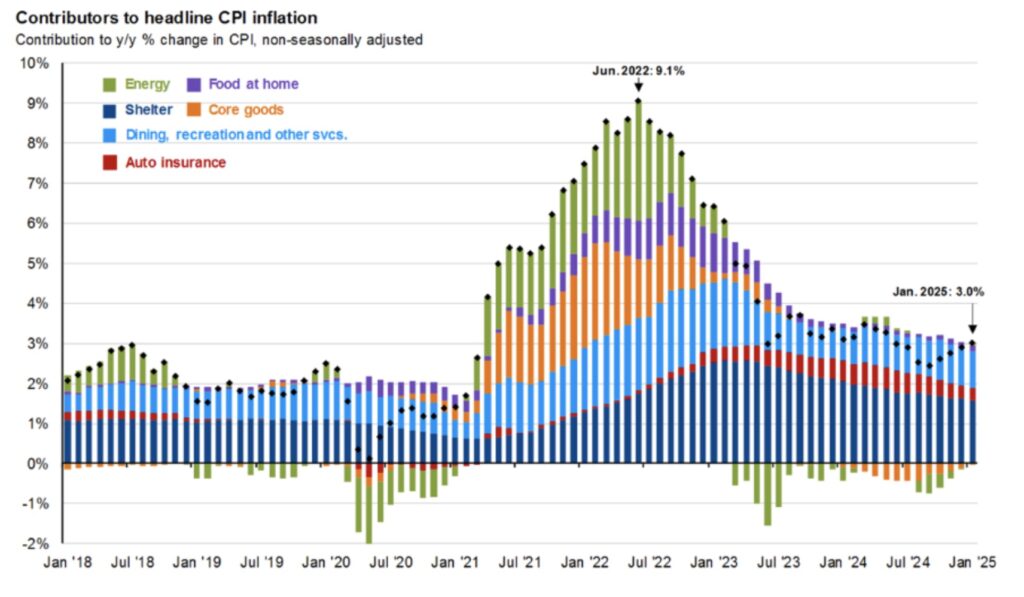

The market is predicting, with a 90% probability, that the Federal Reserve will cut their policy rate by fifty basis points or more by the end of 2025[7]. The Federal Reserve has a dual mandate to maintain price stability and promote maximum employment with the use of monetary policy. As it stands inflation is far from its target and employment, although not at maximum, has shown itself to be stable. Inflation eased a bit over the last twelve months; however, it is proving to be sticky above the Federal Reserve’s 2% target. The Consumer Price Index increased 2.8% year over year in its latest reading at the end of February, within it the shelter index continues to account for most of the level of inflation as seen in figure 3. The unemployment rate has been mostly flat at 4.1% since June of last year[8], however U.S employers announced over 172,000 jobs cuts in February marking the highest monthly total since July 2020[9].

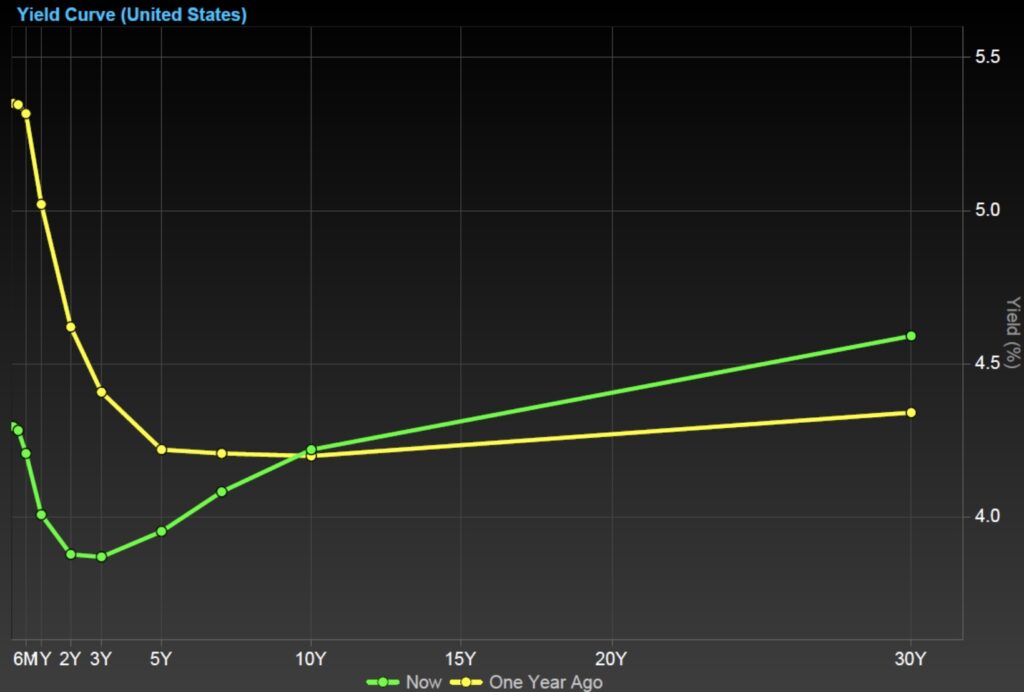

U.S. Treasury yields for mid to long term have decreased since the beginning of the year. The 2-year and 10-year rates both came down nearly forty basis points to 3.9% and 4.2%, respectively[10].

Outlook

The financial markets have experienced notable volatility in recent months, driven by a mix of economic data, central bank policies, and global geopolitical events. The equity markets started off the year as the previous two have finished but have reversed direction as they adjust to the issues addressed above and various levels of uncertainty have been introduced. Bond markets continue to adjust to shifting interest rate expectations, with yields fluctuating as investors assess the policy direction of central banks, both domestically and globally. Commodities, such as oil and gold have seen price swings due to supply chain disruptions and safe-haven demand.

Looking ahead, market sentiment will largely be shaped by monetary policy decisions and economic indicators, particularly inflation and employment data. The Federal Reserve and other central banks are expected to carefully balance growth and inflation concerns, with many investors anticipating potential rate cuts later in the year if inflation eases and/or the economy shows weakness. However, uncertainties remain, including geopolitical tensions, evolving trade policies, and risks of economic slowdown both in the U.S. and internationally.

As potential headwinds and further volatility are expected, the financial markets and investors will most likely focus on inflation trends, employment data, and corporate earnings to gauge the market direction, in the short-term and the remainder of the year.

Always vigilant, our commitment to you is to navigate your portfolio through both calm and turbulent times to work towards your long-term goals and objectives.

Footnote 1, 6: FactSet, data as of 04/02/2025.

Footnote 2: London Stock Exchange – S&P 500 Earnings Scorecard, data as of 03/21/2025

Footnote 3, 5: Fidelity, data as of 04/02/2025.

Footnote 4: JP Morgan Asset Management, FactSet, Standard & Poor’s, data as of 03/31/2025.

Footnote 7: CME Group – FedWatch Tool, data as of 04/02/2025.

Footnote 8: US Bureau of Labor Statistics, data as of 03/31/2025.

Footnote 9: Challenger, Gray, & Christmas Inc.

Footnote 10: CNBC.com, data as of 04/02/2025.

Disclosures

Trust and Portfolio Management services offered by Cypress Bank & Trust are not insured by the FDIC; are not deposits, are not guaranteed; and are subject to investment risks, including possible loss. This does not constitute an offer or solicitation.

This information should not be considered investment advice. Opinions expressed reflect the judgment of the authors and are current opinions as of the date appearing in this material only. While every effort has been made to verify the information contained herein, we make no representations as to its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Past performance does not predict future results. Content should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation. All investing involves risk, including the loss of some or all of your investment.

Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indexes have limitations because indexes have volatility and other material characteristics that may differ from a particular fund.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Information obtained from third party sources is believed to be reliable but has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness, or timeliness of this document.

Specific investments described herein do not represent all investment decisions made by Cypress Bank & Trust. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future.