“Investing is easier than you think, but harder than it looks.”

– Warren Buffett

At this year’s Berkshire Hathaway annual meeting, Warren Buffett announced that he will retire at the end of 2025—marking the close of what is likely the most extraordinary investing career any of us will witness. Over the years, Buffett has shared countless insights and principles, but few are as timeless as the one above.

In this quote, Buffett reminds us that the foundations of sound investing—diversification, patience, and long-term thinking—are not complicated. Yet, what makes investing difficult is managing our own behavior. Emotions like fear, greed, and impatience can quickly derail even the most straightforward strategy.

An important corollary to this idea is Amara’s Law, which states: “We tend to overestimate the effect of a technology in the short run and underestimate the effect in the long run.” We’ve seen this play out time and again—whether with electric vehicles, the internet, or artificial intelligence. Innovations often go through a predictable cycle: the initial burst of enthusiasm, followed by a period of disillusionment, and eventually, a more measured and transformative impact.

For investors, the challenge is recognizing where we are in this cycle—without the benefit of hindsight.

At Cypress Bank & Trust, we aim to address this challenge by constructing and managing client portfolios using time-tested principles. Our disciplined approach emphasizes diversification, patience, and a deep understanding of each client’s goals and circumstances. We don’t chase trends or react to headlines. Instead, we strive to deliver lasting value through thoughtful, long-term strategies.

By staying committed to these principles, we seek to help our clients navigate market turbulence with confidence—always with an eye toward the future they have told us what matters most.

Equities

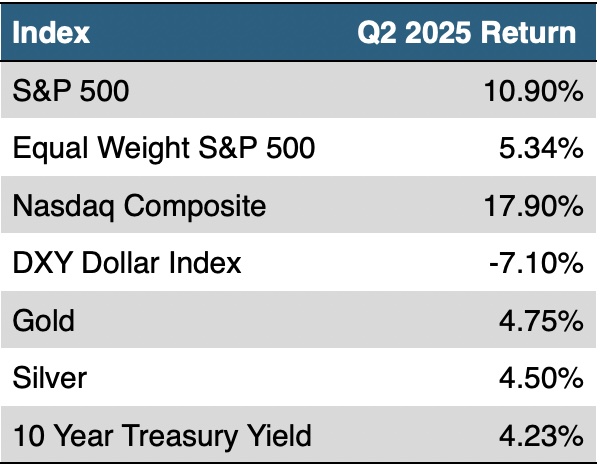

The second quarter of 2025 was marked by heightened volatility in the equity markets, not seen since the second half of 2022. It tested investor conviction but also served to make way for good long-term opportunities. Fueled by the uncertainties imposed by the Tariffs, the S&P 500 hit correction territory and closed at its lowest level this year on April 8th, down 18.9% from its all-time high. By the end of June, the index clawed its way back and reached a new all-time high [1], driven by a potential ceasefire between Israel and Iran, and a looming trade deal with China and other nations. Despite a steep drawdown in early April, the Technology sector finished the second quarter as the best performing sector, returning 23.54%[2]. The Magnificent 7 stocks have returned 18.6% through the second quarter of 2025 outpacing the other 493 companies in the S&P 500 index by nearly 14 percentage points[3].

The Federal Reserve held rates steady in their two meetings this quarter, signaling that interest rate cuts may occur in 2025 if inflation eases and the labor market softens. As much as we have seen the Consumer Price Index easing since the beginning of the year from 3% in January to as low as 2.3% in April’s reading, in the most recent release from the Personal Consumption Expenditure it indicated that inflation has started to creep up as of June[4].

Fixed Income

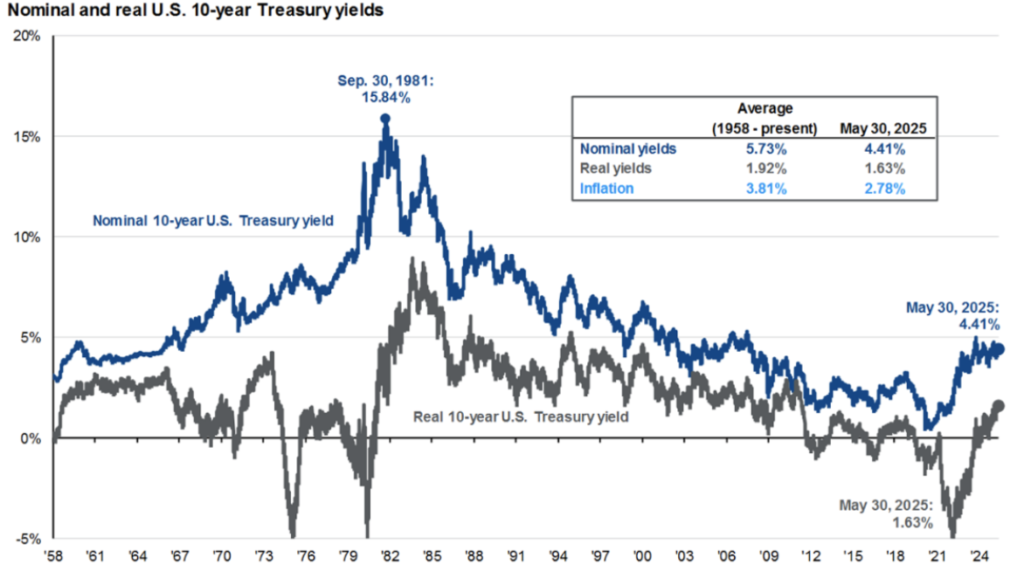

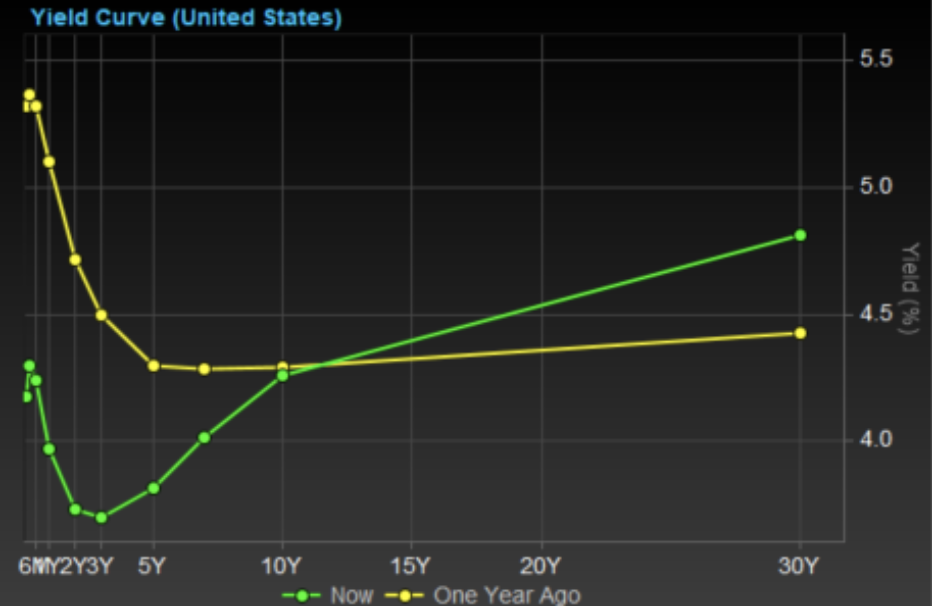

The second quarter saw a high degree of yield swings in the U.S. fixed income markets, as investors had to navigate a terrain marked by rising yields, fiscal concerns, and shifting forecasts around the Federal Reserve’s interest rate policy. Longer maturity U.S. Treasuries sold off, pushing the twenty- and thirty-year yields above 5.1%, levels not seen in years, amid growing concerns over ballooning federal debt and the fiscal budget. As a consequence, long-term Treasuries returned -2.82% during the second quarter as measured by the iShares Twenty-Year Treasury ETF, ticker TLT [5].

Source: FactSet, Tullet Prebon Information. Data as of 06/30/2025.

While the Federal Reserve held rates steady in the second quarter, signaling a cautious path forward, investors began expecting interest rate cuts by September, contingent on how inflation and labor market data evolves until then. This resulted in a bond market that felt like anything but a safe haven with higher-than-normal volatility.

Outlook

As we enter the second half of 2025, the financial markets continue to navigate a landscape shaped by cooling inflation, stable economic growth, and the Federal Reserve’s anticipated policy shift. With inflation steadily trending lower, the Fed is widely expected to implement one or two interest rate cuts before year-end. This easing cycle, coupled with resilient consumer and business activity, provides a constructive backdrop for both stock and bond markets—though geopolitical risks and the execution and implementation of tariff policy will add near-term volatility.

Equity markets have been largely supported by strong earnings and investor optimism, particularly in the technology sector. Looking ahead, we expect market leadership to broaden. Companies with healthy balance sheets, strong cash flow, and the ability to adapt to shifting conditions will continue to stand out.

In the fixed income space, higher yields are offering more compelling opportunities than we’ve seen in recent years. Investors are finding value across high-quality bonds, including Treasuries, municipals, and investment-grade corporates. Overall, staying diversified, maintaining a long-term perspective, and focusing on quality will be key strategies for navigating the months ahead.

Always vigilant, our commitment to you is to navigate your portfolio through both calm and turbulent times to work towards your long-term goals and objectives.

Footnote 1: Reuters.com, S&P 500, Nasdaq close at record highs. Published on 06/30/2025.

Footnote 2: Fidelity Sector Returns, data as of 07/01/2025.

Footnote 3: J.P. Morgan Asset Management, Review of markets over Q2 of 2025.

Footnote 4: U.S. Bureau of Labor Statistics, data as of 06/30/2025.

Footnote 5: FactSet Research Systems, data as of 07/01/2025.

Disclosures

Trust and Portfolio Management services offered by Cypress Bank & Trust are not insured by the FDIC; are not deposits, are not guaranteed; and are subject to investment risks, including possible loss. This does not constitute an offer or solicitation.

This information should not be considered investment advice. Opinions expressed reflect the judgment of the authors and are current opinions as of the date appearing in this material only. While every effort has been made to verify the information contained herein, we make no representations as to its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Past performance does not predict future results. Content should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation. All investing involves risk, including the loss of some or all of your investment.

Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indexes have limitations because indexes have volatility and other material characteristics that may differ from a particular fund.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Information obtained from third party sources is believed to be reliable but has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness, or timeliness of this document.

Specific investments described herein do not represent all investment decisions made by Cypress Bank & Trust. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future.