“It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of light, it was the season of darkness, it was the spring of hope, it was the winter of despair.”

― Charles Dickens, A Tale of Two Cities

While Dickens was contrasting the lives of three families in London and Paris during the French Revolution, we think he could easily have been describing the stock market in 2024. For investors who owned a small select group of stocks (specifically Nvidia, Taiwan Semiconductor, Eli Lilly, Broadcom & Qualcomm) your return so far in 2024 is in excess of 70%. If on the other hand you owned the Dow Jones Industrial Average your return year to date is 5%, which pales in comparison.

For the year, the S&P 500 is up 15% and it is commonly known that Nvidia, Microsoft, Meta, Alphabet, Amazon, and Apple account for over 60% of the S&P 500’s year to date gain. What is less well known is that the average stock is priced about where it was at the start of 2022.

As a result of their epic move, Nvidia, Microsoft and Apple now account for over 20% of the entire S&P 500 market capitalization. Historically this type of market concentration has proven to be an inflection point in the market. Only time will tell if this time will be different or not but we at Cypress Bank & Trust are not sitting on our hands. We expend a significant amount of time and energy not only researching the positions to add to our clients’ portfolios but also quite a bit of time evaluating the existing holdings in our clients’ portfolios.

In this way we can properly weigh potential risks and return opportunities that the markets, asset classes and specific securities offer our clients. The outcome is a customized portfolio that is bespoke for each client so we aim to achieve the specific goals and characteristics tailored to each client.

As such we are better able to position our clients’ portfolios over a wide ranging variety of market outcomes because our experience has taught us that no matter how optimistic or pessimistic the market is about future events just as we saw in A Tale of Two Cities, things are not always what they seem and it is our commitment to our clients to endeavor to discern the difference.

Equities

The U.S. stock market has continued its upward trajectory during the second quarter. The S&P 500 index closed the quarter at an all-time high for the second quarter in a row. The S&P 500 was up 4% in the second quarter, taking the year-to-date return to over 15%. The Nasdaq Composite, which has a high exposure to Technology, had a return of 8% for the quarter while the Dow Jones Industrial Average retreated nearly 2%.

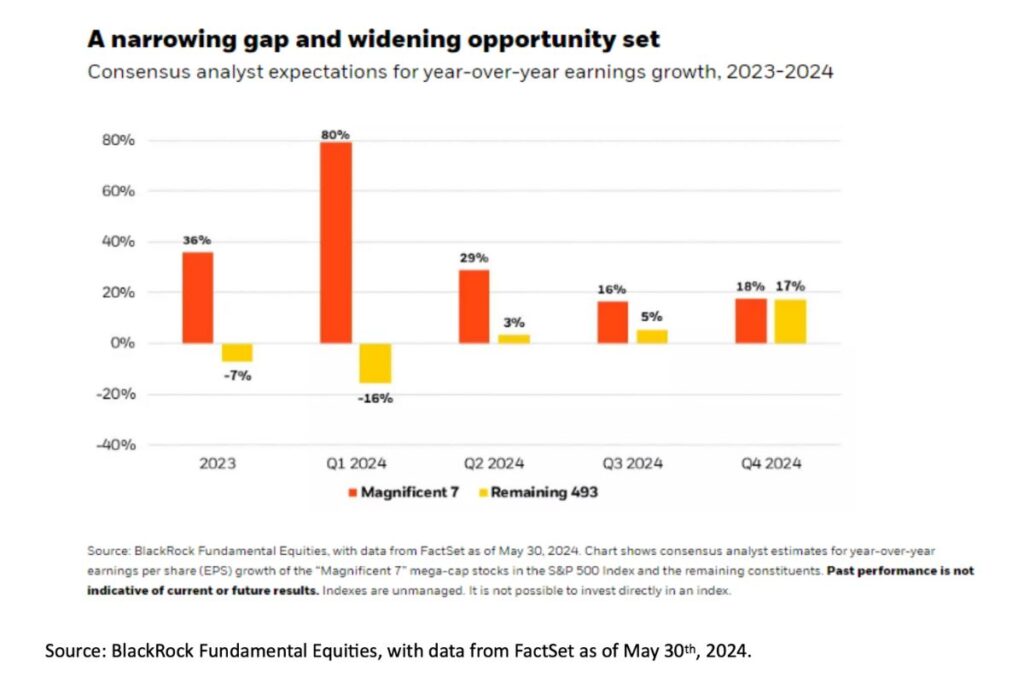

In Q1 of 2024, the S&P 500 saw their earnings grow 5.9% year over year. Identical to the Q4 of 2023, the sectors with double digit growth in Q1 of 2024 were Communication Services, Consumer Discretionary, Utilities, and Technology. However, Materials, Healthcare, and Energy sectors saw negative earnings growth. The variance between the top and bottom performing sector was 59%. As for revenues, the spread was much narrower at 16%. Of the 11 sectors, 8 saw positive revenue growth ranging from 3% to 8%.

In this first half of 2024, we have seen the concentration further increase in the S&P 500. The Magnificent 7 (composed of Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta Platforms, and Tesla) had a 33% return year to date, while the S&P 500 ex-Magnificent 7 had returns of a mere 5%. The Invesco S&P 500 Equal Weight ETF (Exchange Traded Funds) also returned 5% for the first half, while retreating 3% in the most recent Q2.

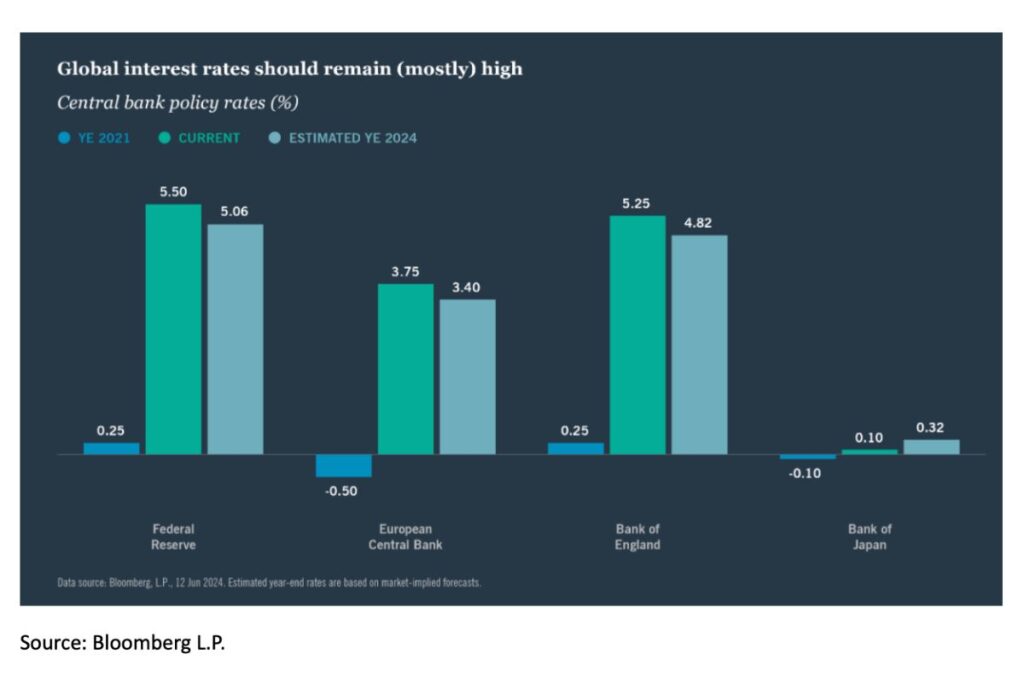

There is optimism the Federal Reserve will finally start cutting interest rates this year as early as September. To offset this optimism, geopolitical tensions are still high along with the looming presidential elections in the US and globally, in which many market impacting issues are up for debate.

Fixed Income

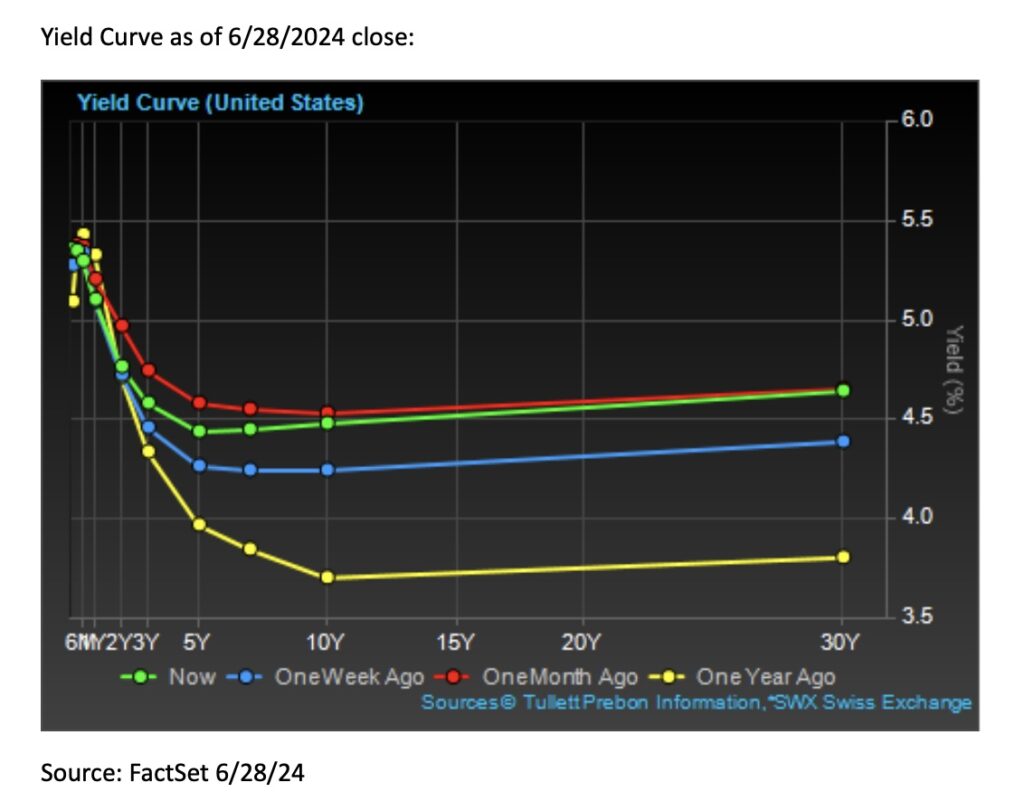

Treasury yields displayed heightened volatility in the beginning of the second quarter, as inflation figures for the beginning of the year were hotter than expected. The Federal Reserve (the Fed) held two meetings in this past quarter where it decided to hold interest rates steady. However, during their May meeting, the Fed announced a decrease in the speed of its balance sheet runoff by shrinking the current cap of $60 billion to $25 billion per month of US Treasury securities it lets mature and not be replaced. The Fed’s balance sheet runoff is often referred to as quantitative tightening (QT), and as the name implies it is meant to decrease excessive liquidity in the economy. The change in the runoff cap by the Fed is aimed at decreasing the pace of QT and keeping longer term interest rates more stable as the Fed only has control over short-term rates. In their June meeting, the Federal Reserve released the “dot plots” (the expected path for rates) where it targeted one cut by the end of 2024, a shift from their previous expectations of three cuts.

The unemployment rate increased during the second quarter, although it has only done so incrementally from 3.9% to 4% in the last reading. In terms of inflation, we have seen it come down drastically from 2022 where it was as high as 9%, but it has been stuck around 3% since the summer of 2023. The interest rate path forward will depend on several factors, the two most important being inflation and employment levels.

Outlook

Predictions of a recession have come in waves through the last 3 years, and yet here we still stand. While the scare of a recession is still afloat, it has reasonably retreated in these past six months. On one side of the coin, inflation figures have substantially improved, unemployment remains below the historical average, and the stock market is continually topping its all-time highs. The other side of the coin is a bit grimmer as geopolitical risk remains high, inflation is proving to be sticky at around 3% which is above the Fed’s 2% target, and the stock market is breaking records in concentration risk and high valuations multiples. At last, we still have an election in November which has implications in taxes, government spending, and global trade. So, where does our economy go from here? Here at Cypress Bank & Trust, we maintain investors should stay focused on the long-term and maintain adequate diversification to help them navigate these uncertainties.

Always vigilant, our commitment to you is to navigate your portfolio through both calm and turbulent times to work towards your long-term goals and objectives.

We hope you and your family have a healthy and fulfilling summer!!!

Disclosures

Trust and Portfolio Management services offered by Cypress Bank & Trust are not insured by the FDIC; are not deposits, are not guaranteed; and are subject to investment risks, including possible loss. This does not constitute an offer or solicitation.

This information should not be considered investment advice. Opinions expressed reflect the judgment of the authors and are current opinions as of the date appearing in this material only. While every effort has been made to verify the information contained herein, we make no representations as to its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Past performance does not predict future results. Content should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation. All investing involves risk, including the loss of some or all of your investment.

Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indexes have limitations because indexes have volatility and other material characteristics that may differ from a particular fund.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Information obtained from third party sources is believed to be reliable but has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness, or timeliness of this document.

Specific investments described herein do not represent all investment decisions made by Cypress Bank & Trust. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future.