Is the Federal Reserve on the horns of a dilemma?

Ever since the Federal Reserve began raising interest rates in March of 2022 Wall Street pundits have been anticipating the eventual easing of interest rates by the Federal Reserve. Over the past twelve months the collective market punditry has speculated that the Federal Reserve will cut rates from zero to seven times this year. Now that the Federal Reserve has begun to cut interest rates at their last meeting in September two questions need to be asked:

1. Are additional rate cuts necessary?

2. If so, then how many?

Many economic statistics indicate the economy is slowing down, and the Federal Reserve needs to act before more economic damage is incurred. On the other hand, there are just as many economic statistics that indicate that the economy is not in a recession and in fact has been growing, albeit slowly, consistently for the past number of quarters.

As of last quarter, U.S. household wealth rose at almost a 7% annual rate (double the pace of disposable income growth) to a record $184.5 trillion driven primarily from gains in real estate and the stock market. At the same time credit card delinquency rates have doubled off the lows from Q3 2021 and Americans owe a record $1.14 trillion (about $3,500 per person in the US) on their credit cards.

Although unemployment has risen to 4.2% from 3.5% and the number of unemployed people stands at 7.1 million so far this year, there have been almost 1.5 million jobs created.

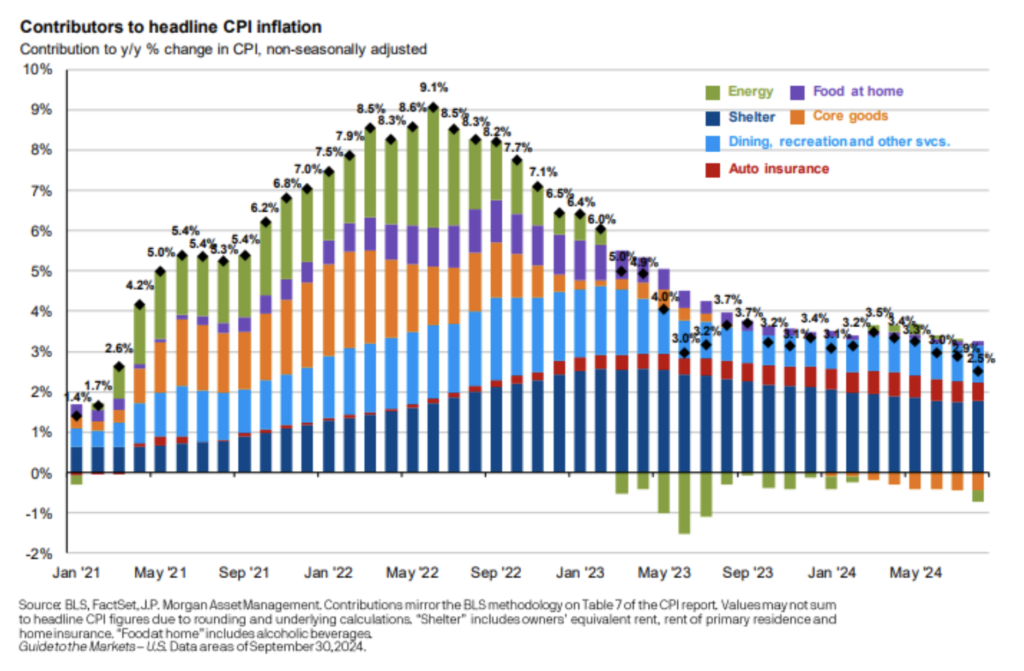

Inflation as measured by the Consumer Price Index has fallen from over 9% annually to 2.5% over the last 12 months. Although the Federal Reserve has a stated 2% annual goal for inflation many members have stated a desire to have additional rate cuts before year end and into 2025.

While some might argue for a significant number of rate cuts there are many who would prefer that the number of rate cuts be kept at a minimum. The impact of these potential cuts will impact not only the stock market but also the amount of interest that investors can earn along with the price of real estate and other assets in addition to the overall economy.

As the Federal Reserve wrestles with this dilemma, we at Cypress Bank & Trust are diligently evaluating the various market forces that can impact our clients’ portfolios and aiming to determine how to best position them so that we can take advantage of the potential opportunities that the markets present. There is no single investment or portfolio that is right for every investor, that is why we seek to tailor our solutions for each client’s specific needs and goals.

Equities

The third quarter roller coaster has finally come to a halt. Although the mood of investors ended the quarter on a positive note, let’s not forget how we got here. The stock market, as measured by the S&P 500 Index, finished Q3 with a 5.6% return for the quarter and a 22% return year to date. However, in early August we witnessed the S&P 500 have its largest single day drop of 3% in nearly two years because of the Japanese Yen carry trade unwind. Some market participants were even calling for an emergency interest rate cut from the Federal Reserve, an act that we have seen happen twice in the past 20 years; during the Great Financial Crisis in 2008 and the Covid-19 pandemic in March of 2020. The markets did calm down and returned to their positive trajectory once economic data releases, like the Consumer Price Index (CPI) and the Personal Consumption Expenditures Index (PCE), showcased the inflation rate moving towards its 2% target. On their September 18th Federal Open Market Committee meeting, the Federal Reserve did begin its much-anticipated interest rate cutting cycle with a large 50 basis point cut, a move that saw the S&P 500 rally nearly 3% in these last two weeks of the quarter. Market gyrations can be overwhelming if looked at within a short time frame and that’s why here at Cypress Bank & Trust we believe in staying invested for the long term as the best chance of achieving your return goals.

Market rotation was another big theme during Q3, as some of the underperforming sectors and pockets of the market exhibited overperformance during this quarter. The equal weighted S&P 500 had nearly double the return of the market weighted index at 10.4% for Q3 as measured by the Invesco S&P 500 Equal Weight ETF (RSP). We also saw the semiconductor industry have a return of -5% for the quarter, measured by the VanEck Semiconductor ETF (SMH), against a return of over 10% for the Russell 2000 Index (Mid and Small caps). Lastly, the top three performing sectors in Q3 were Utilities, Real Estate, and Industrials returning 19.4%, 15.5%, and 11.1%, respectively, while the bottom 3 sectors were Technology, Energy, and Communication Services with returns of -1.25%, -0.95%, and 1.82%, respectively.

Fixed Income

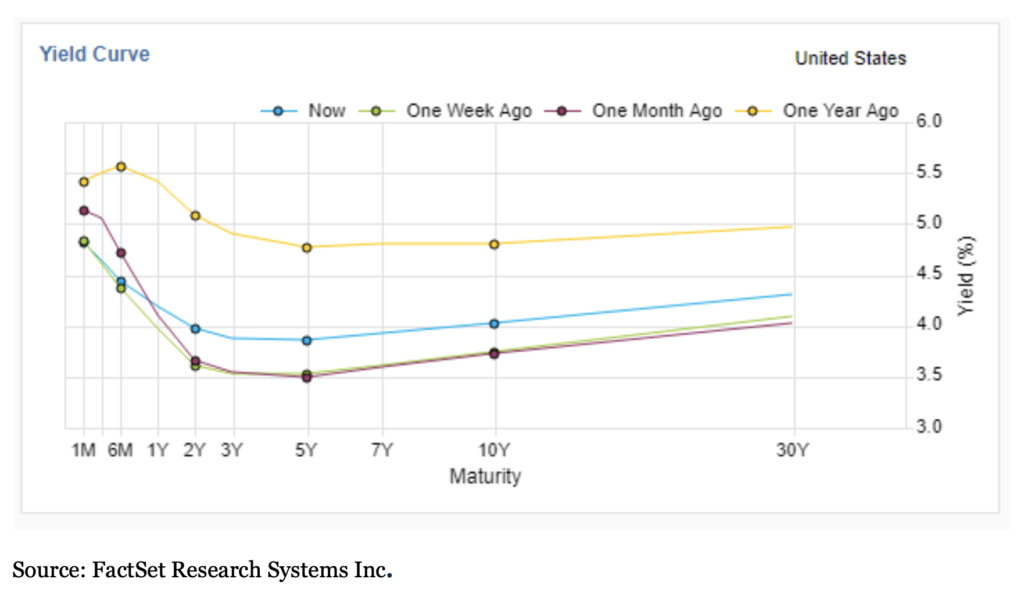

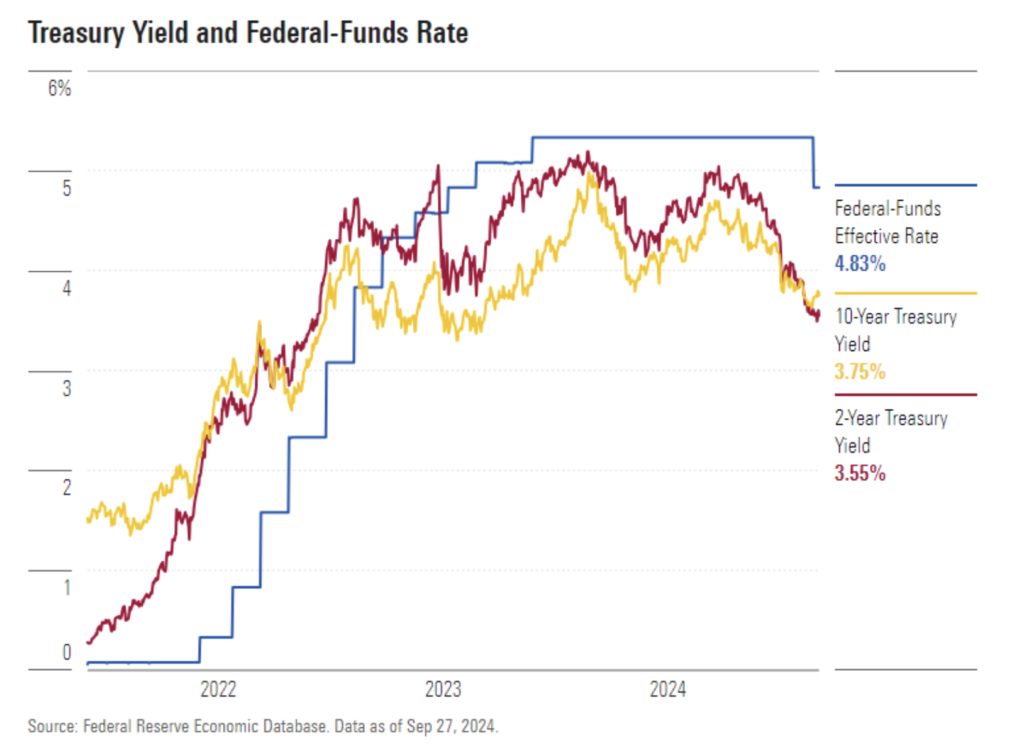

The Treasury yield curve has been inverted (2-year yields being higher than the 10-year yields) for the longest stretch of time on record since July of 2022. An inverted yield curve has historically been a sign that a recession is looming, however; one has not yet arrived. In August of this year, the yield curve finally normalized as expectations of an interest rate cut increased after a series of good inflation data and weakening labor markets reports were released.

The Federal Reserve did indeed cut their benchmark rate by 50 basis points, to the surprise of many, to take their current target range from 4.75% to 5%. There are expectations that the Federal Reserve will continue to move on with its cutting rate cycle through the rest of 2024 and into the first few meetings of 2025.

Congruent to the Equity markets, gains in the broad Fixed Income markets continued to pile on during the third quarter. Yields on Treasury notes for all durations fell throughout the third quarter. As yields fell bonds had some price appreciation, the Bloomberg US Aggregate Index (the most used fixed income index in the US) gained 5.8% for Q3, and over the past 12 months it has gained 11.6%.

Outlook

As we look ahead to the next quarter, the market outlook reflects a mix of cautious optimism and underlying challenges. Economic indicators suggest moderate growth, driven by consumer spending and a resilient labor market. However, inflationary pressures continue to influence monetary policy, with potential for interest rate adjustments that could impact borrowing costs and consumer confidence. Investors are closely watching central bank signals, which will play a crucial role in shaping market sentiment.

Additionally, geopolitical tensions and supply chain disruptions remain significant factors that could introduce volatility. The upcoming election may also introduce uncertainty into the markets. We will stay informed and adaptable, considering both opportunities and risks as we approach this final quarter of 2024, and the calendar turns to 2025.

Always vigilant, our commitment to you is to navigate your portfolio through both calm and turbulent times to work towards your long-term goals and objectives.

Disclosures

Trust and Portfolio Management services offered by Cypress Bank & Trust are not insured by the FDIC; are not deposits, are not guaranteed; and are subject to investment risks, including possible loss. This does not constitute an offer or solicitation.

This information should not be considered investment advice. Opinions expressed reflect the judgment of the authors and are current opinions as of the date appearing in this material only. While every effort has been made to verify the information contained herein, we make no representations as to its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Past performance does not predict future results. Content should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation. All investing involves risk, including the loss of some or all of your investment.

Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indexes have limitations because indexes have volatility and other material characteristics that may differ from a particular fund.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Information obtained from third party sources is believed to be reliable but has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness, or timeliness of this document.

Specific investments described herein do not represent all investment decisions made by Cypress Bank & Trust. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future.