Time to Hunker Down

One of the many lessons learned from living in Florida is that every year brings with it Hurricane Season. At the start of each season, weather experts run their models, weighing countless variables and historical patterns, to forecast how many storms may develop and how many might become hurricanes. Some years, the storms fizzle and we are spared the worst. Other years, their models prove prescient, and people in the path of nature’s wrath face devastating consequences.

The stock market often presents a similar dynamic. At the risk of sounding like “Chicken Little,” we see a set of conditions today that give us pause. These factors do not guarantee a storm is coming, but they do warrant greater vigilance. Specifically, three stand out:

i. Valuation

The S&P 500 is trading at a Cyclically Adjusted Price-to-Earnings (CAPE) ratio above 38 for three consecutive months. In the past century, this has only happened twice — in 1999 and late 2021. Historically, this ratio ranges between 15 and 22(1).

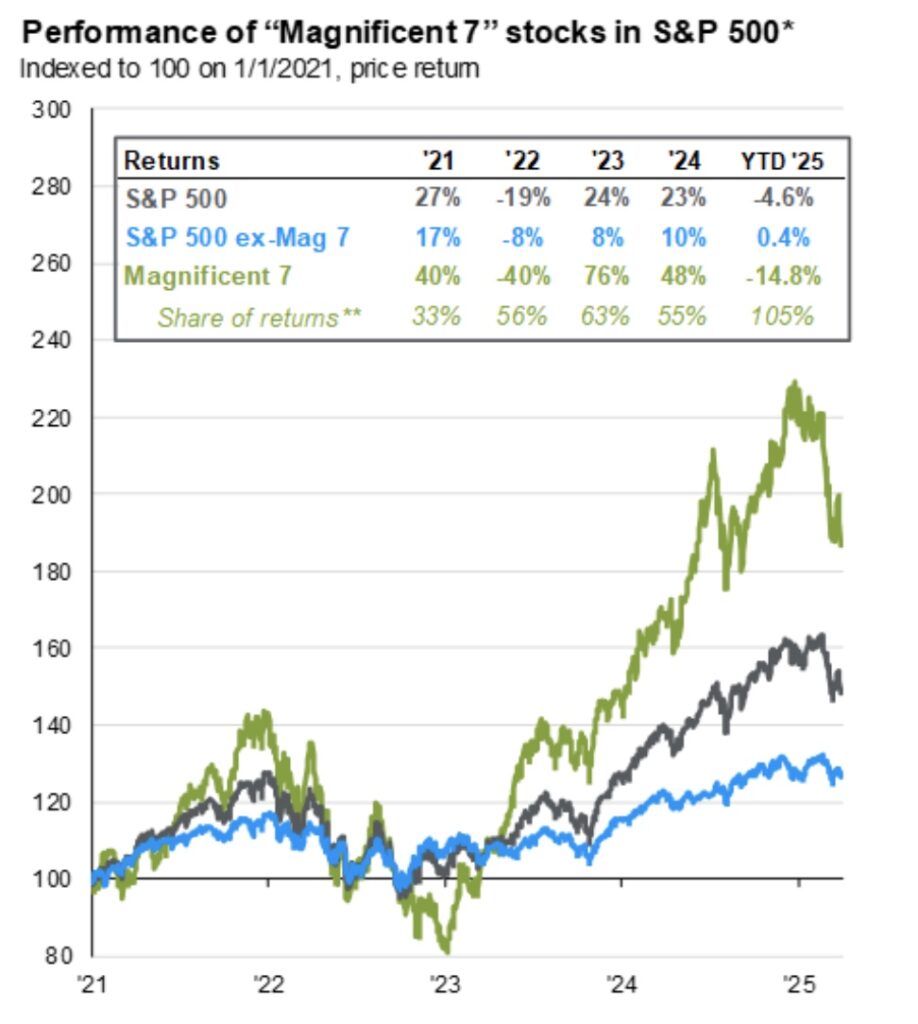

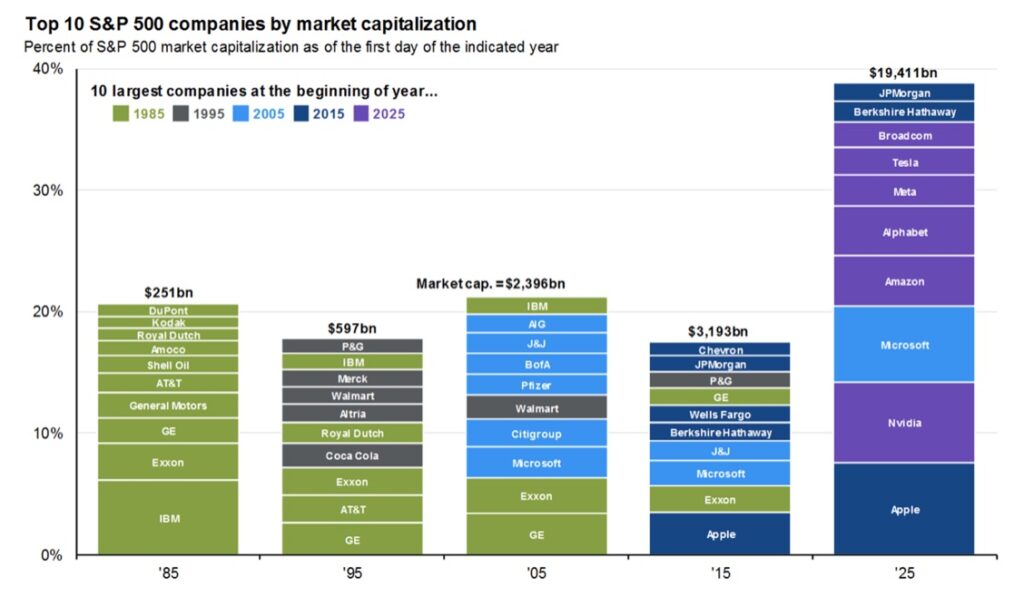

ii. Market Concentration

The top ten stocks now account for nearly 38% of the S&P 500, compared with a historical range of 20–25%. Earnings growth has also narrowed, with Information Technology and Communication Services responsible for 70% of S&P earnings growth since late 2022 and 90% over the past year (2).

iii. Leverage

Margin debt — credit extended against marketable securities — has surpassed $1 trillion. It has grown 33% in the past year, nearly twice the pace of the S&P 500 itself (3).

Like hurricane forecasts, these signals do not tell us precisely when or if a market storm will arrive. What they do suggest is that the conditions are in place. At Cypress Bank & Trust, our role is to prepare clients to withstand whatever comes.

Our investment philosophy is never to be “all in” or “all out.” Instead, we manage portfolios that balance risk and reward in the context of each client’s individual circumstances, income needs, and long-term goals. By budgeting for risk and structuring portfolios with resilience, we help clients weather the inevitable storms and continue on the path toward their objectives.

Equity Market

The U.S. equity market delivered robust gains in the third quarter, with all major indexes including the S&P 500, Nasdaq Composite, and Dow Jones Industrial Average reaching new record highs. This rally was fueled by several key factors: stronger-than-expected Q2 earnings, sustained momentum in artificial intelligence (AI) across semiconductors and the broader tech sector, growing expectations of Federal Reserve rate cuts later in the year, and a swift rebound from the tariff-driven selloff in April (4).

Technology led the third quarter sector performance with a 14% return, followed by Communications, which gained 12%. The continued acceleration of AI innovation and investment was a major catalyst, with mega-cap tech firms like Apple, Alphabet, and Nvidia driving much of the upside (5).

On the currency front, the U.S. Dollar Index (DXY) declined 9.5% year-to-date, reflecting broad weakness against major global currencies. This depreciation supported gains in hard assets, particularly precious metals. Silver stood out with a 28% surge, benefiting from both safe-haven demand and strong industrial usage. Gold also posted a solid 16% quarterly gain, climbing to a record high above $3,800 per ounce, as investors sought protection amid geopolitical tensions and concerns over elevated equity valuations (6).

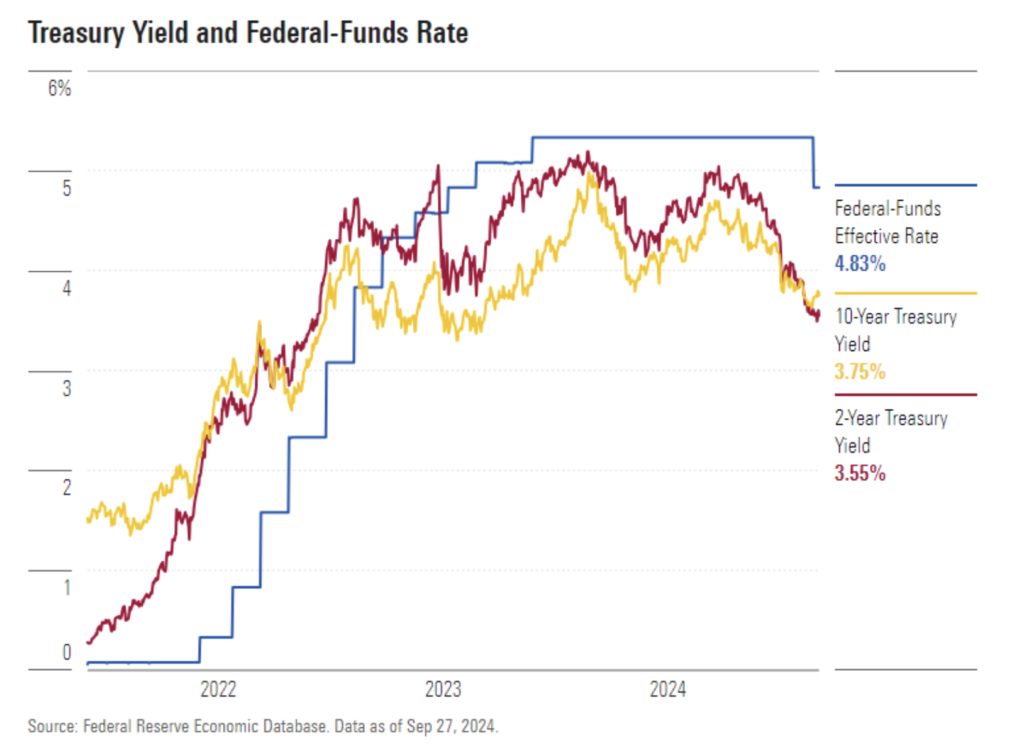

Fixed Income

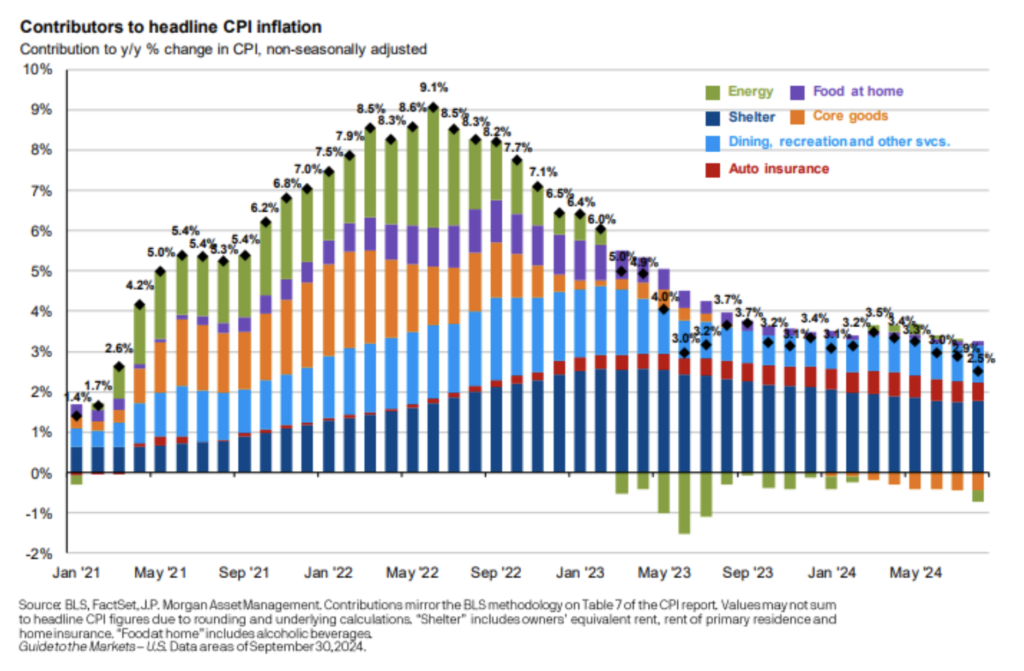

In a widely anticipated move, the Federal Reserve lowered its benchmark interest rate in September for the first time in a year, adjusting the target range to 4.00%–4.25%. This shift toward a more accommodative stance was driven by growing signs of labor market weakness, although inflation measures are proving sticky above the Federal Reserve 2% target. The rate cut provided a clear boost to fixed income markets, reinforcing expectations that the Fed will continue easing at a measured pace into 2026. Current projections by analysts and investors suggest the policy rate could settle between 3.0% and 3.5%, as officials weigh persistent inflation pressures against a softening employment backdrop (7).

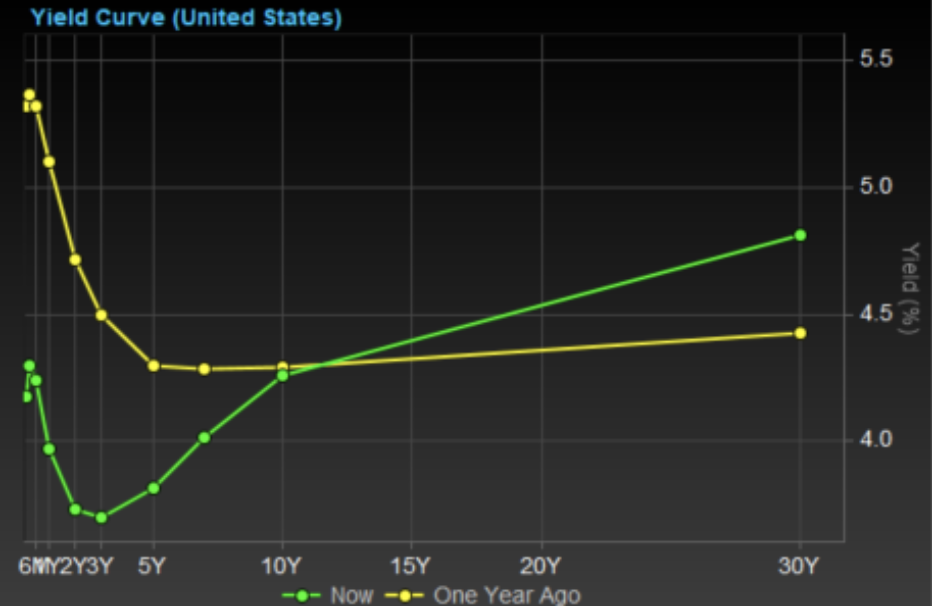

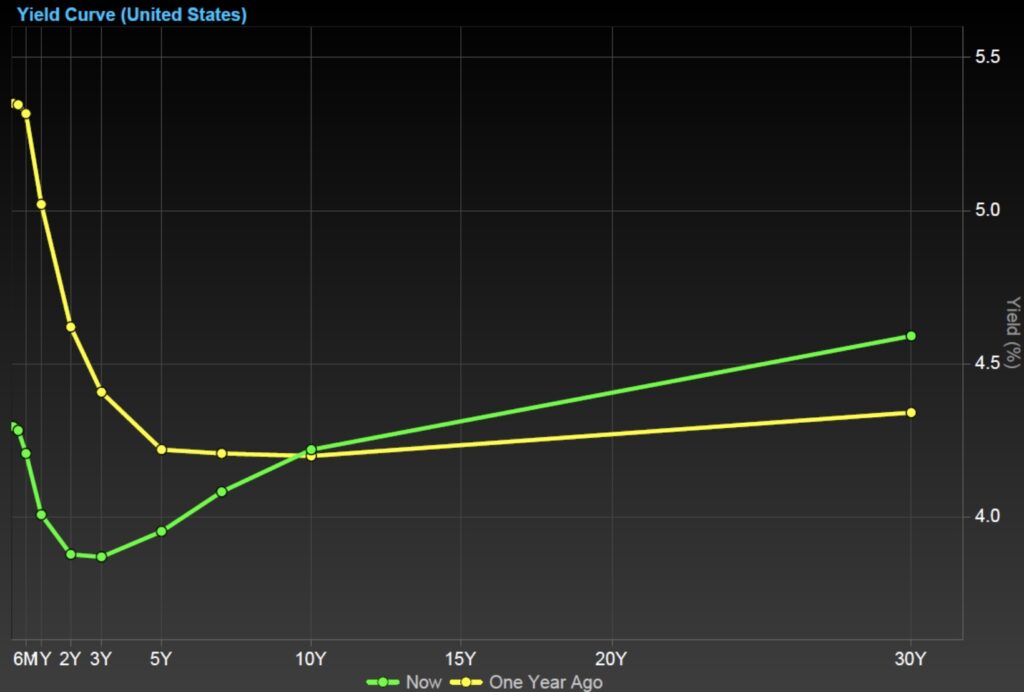

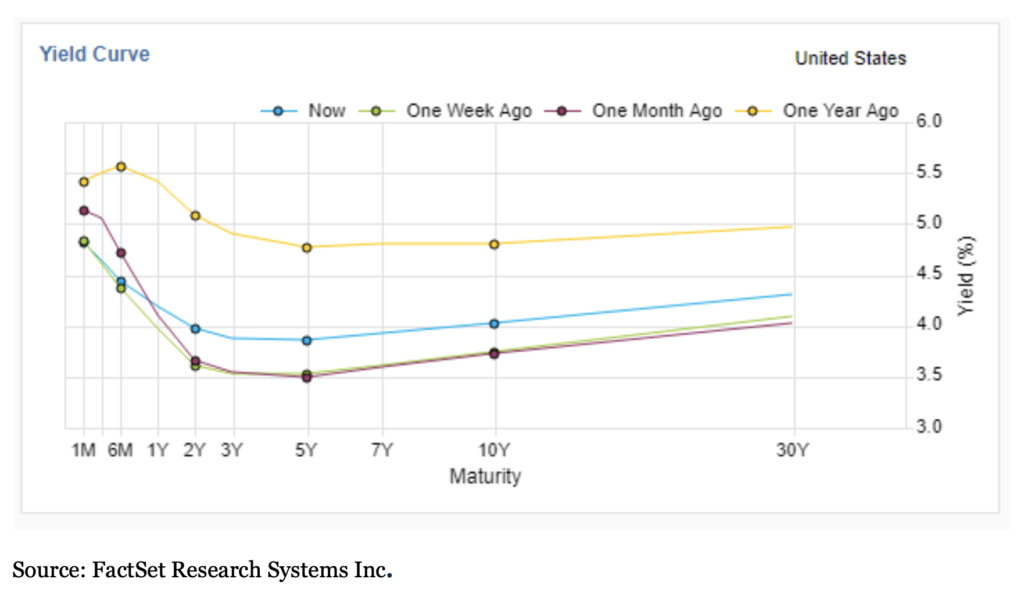

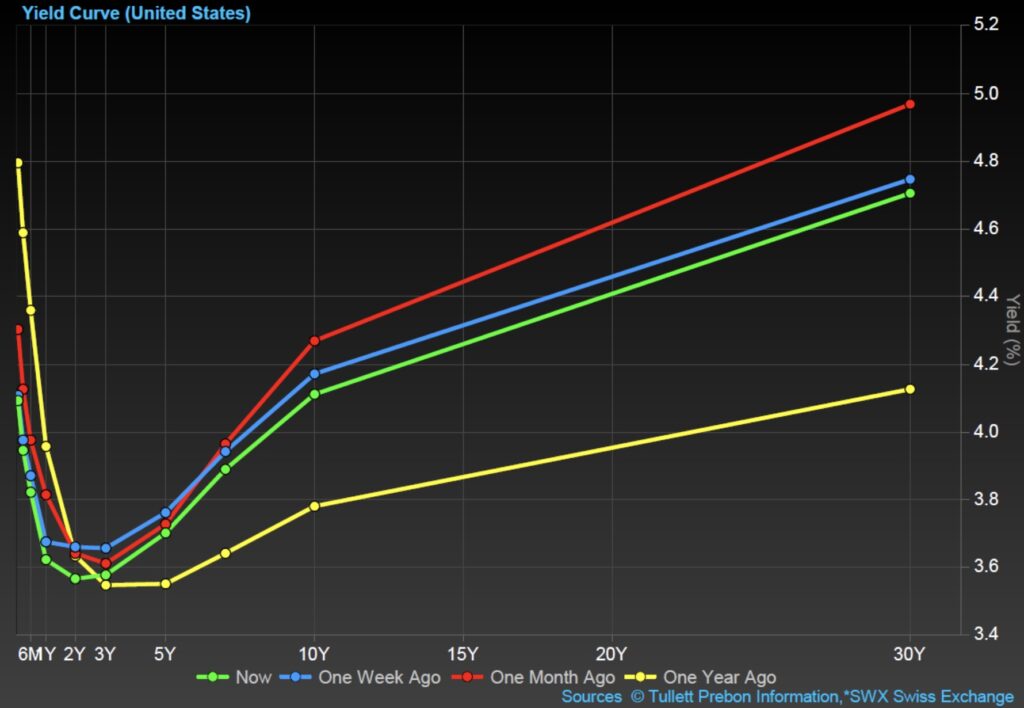

Treasury yields declined across the curve during Q3, contributing to a steepening yield curve. The 10-year Treasury yield ended the quarter near 4.10%, while the 2-year yield fell to 3.54%, reflecting expectations of further rate cuts. Meanwhile, the 30-year yield remained elevated for most of the third quarter, hovering around 5% before closing at 4.7%, driven by concerns over long-term fiscal sustainability and policy uncertainty (8).

Outlook: Q4 2025 and Beyond

As we enter the final quarter of 2025, financial markets are showing signs of cautious optimism. U.S. equities continue to perform well, particularly in the technology sector, driven by strong earnings and sustained investment in AI infrastructure. While inflation has moderated, global trade tensions and sector-specific headwinds—especially in manufacturing and diagnostics—are contributing to volatility. Ongoing monitoring of interest rate trends and geopolitical developments should dominate the headlines in the short term and be key drivers of the market’s direction.

Looking ahead to 2026, the outlook remains constructive. Analysts anticipate continued strength in U.S. equities, supported by easing monetary policy and robust consumer demand. The Federal Reserve is expected to maintain its rate-cutting trajectory, which could stimulate investment and support valuations across sectors. With the major markets near or at all-time highs, support from monetary and/or fiscal policy may not only be needed, but it may also already be priced in. However, risks such as persistent services inflation, wage pressures, and global policy uncertainty—particularly around U.S.-China trade relations—may impact margins and investor sentiment.

While short-term market fluctuations and macroeconomic uncertainties—such as inflation persistence and global trade tensions — may create volatility, we encourage clients to stay focused on their long-term financial goals. Diversification remains a key strategy for managing risk and smoothing returns across changing market conditions. By maintaining a disciplined approach and resisting the urge to react to short-term noise, investors can better position themselves to benefit from long-term growth opportunities. Our team is here to help you evaluate your portfolio, ensure alignment with your objectives, and make thoughtful adjustments as needed to navigate the road ahead with confidence.

Always vigilant, our commitment to you is to navigate your portfolio through both calm and turbulent times to meet your long-term goals and objectives.

Sources:

(1) Gurufocus.com; Ycharts.com. S&P 500 Shiller CAPE Ratio

(2) FactSet Earnings Insight 10/03/2025; FactSet Dashboard

(3) First Trust, Three on Thursday, 07/31/2025

(4) Yahoo.com, Dow, S&P 500, Nasdaq notch records on AI buzz even as government shutdown drags on, 10/02/2025

(5) Fidelity.com, Sector Returns, 10/01/2025

(6) FactSet Dashboard, 10/01/2025

(7) CME Group, CME FedWatch Tool, 10/01/2025

(8) CNBC.com, https://www.cnbc.com/bonds/

Disclosures

Trust and Portfolio Management services offered by Cypress Bank & Trust are not insured by the FDIC; are not deposits, are not guaranteed; and are subject to investment risks, including possible loss. This does not constitute an offer or solicitation.

This information should not be considered investment advice. Opinions expressed reflect the judgment of the authors and are current opinions as of the date appearing in this material only. While every effort has been made to verify the information contained herein, we make no representations as to its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Past performance does not predict future results. Content should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation. All investing involves risk, including the loss of some or all of your investment.

Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indexes have limitations because indexes have volatility and other material characteristics that may differ from a particular fund.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Information obtained from third party sources is believed to be reliable but has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness, or timeliness of this document.

Specific investments described herein do not represent all investment decisions made by Cypress Bank & Trust. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future.